Diamond Market Statistics 2024

Published: 23.08.2023 Updated: 27.12.223Main figures and facts:

1. The global polished diamond market is projected to reach $100 billion in 2023.

2. A staggering 54% of the worldwide consumer market for polished diamonds is firmly under the United States’ sway, positioning it as a commanding force in the industry.

3. A groundbreaking shift is underway, as more than half of polished diamonds sold in the U.S. since the summer of 2023 originate from labs. This market share is poised for expansion in the near future.

4. Amidst this transition, prices of lab-grown polished diamonds have witnessed a substantial decline of up to 60% during the 2021-2023 period. In contrast, prices of natural polished diamonds have undergone minimal fluctuations.

5. However, in 2023, natural diamond prices also showed a negative trend. Thus, in the 12 months from December 2022 to December 2023, depending on the size and shape, prices for natural diamonds decreased from 10% to 40%. Curiously enough, prices for the smallest (melee) diamonds, that are typically used for accenting larger stones in jewellery, remained almost unchanged. But the most popular sizes – 0.5 and 1 carat – fell in price by up to 30%.

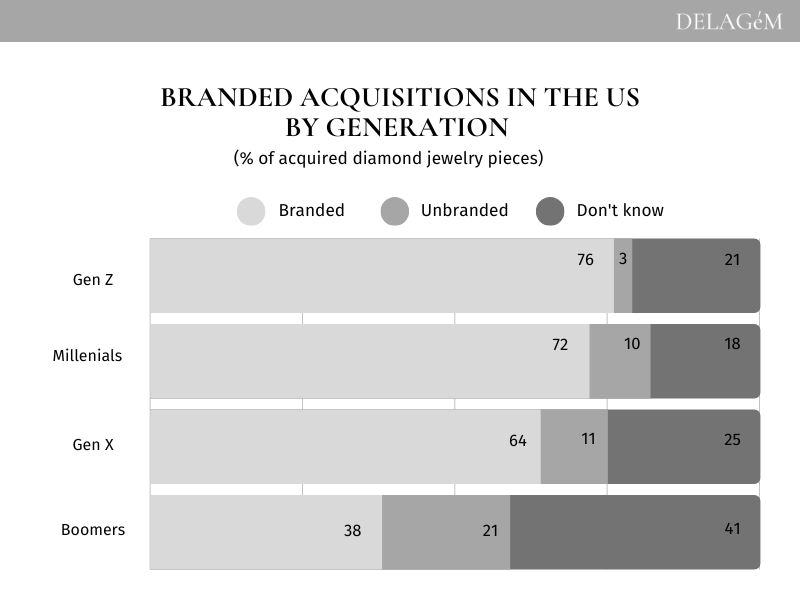

6. Discerning a pattern, young and high-income consumers have demonstrated a preference for branded diamond jewelry, accounting for nearly 75% of their choices.

7. Despite the evolving market, the global demand for diamond jewelry has experienced a decline of 5-17% across various countries in 2023, measured by volume.

Global Diamonds Market Volume

■ The diamond market is set to embark on a captivating journey, surging by a remarkable USD 39,665 million from 2022 to 2027, with an impressive Compound Annual Growth Rate (CAGR) of 8.04% throughout this period. The global diamond market size was USD 97.10 Billion in 2022. The projected Year-over-Year growth rate for 2023 stands at 6.94%. (Technavio, 2023)

■ The diamond industry rebounded spectacularly in 2021 following a slump in 2020 due to the Covid-19 pandemic. This rebound encompassed a 62% surge in revenue within the diamond mining sector, a 55% uptick in cutting and polishing, and a 29% rise in diamond jewelry retail — a triumphant resurgence beyond pre-pandemic levels by +13%, +16%, and +11%, respectively. (Bain, 2022)

■ Notably, the global diamond jewelry market’s valuation skyrocketed to an impressive USD 87 billion in nominal terms during 2021, marking a noteworthy USD 19 billion augmentation from the previous year.

■ The latter part of 2022 and the ongoing year of 2023 have unveiled a market landscape marred by declining fundamentals. The summer of 2023 witnessed major mining entities report a reduction in rough diamond production due to waning demand, leading to a substantial 44% plunge in sales. (Read more here)

Geography of Production of Natural Diamonds

■ The global stage witnessed the extraction of a staggering 116 million carats of diamonds from mines during 2021. Powerhouse contributors to this substantial output include Australia, Canada, the Democratic Republic of Congo, Botswana, South Africa, and Russia.

■ The tapestry of diamond reserves paints a vivid picture, with estimates hovering around an impressive 1.3 billion carats. Among these, Russia claims the crown, boasting the world’s largest diamond reserves, clocking in at around 600 million carats. (Statista, 2023)

■ Russia’s towering presence in diamond production was evident in its staggering output of 41.92 million carats in 2022, positioning it as the undisputed leader on the global diamond mining stage. However, a nuanced narrative emerges as Russia’s prominence undergoes transformation, raising questions about its future stature.

Russia’s rough-diamond exports experienced a substantial 24% decline in 2022, plummeting to 36.7 million carats, a consequence of stringent import restrictions imposed by governments globally.

■ A looming challenge for the diamond industry is the anticipated shortage of natural diamonds. As demand escalates while known global diamond reserves deplete, a conspicuous diamond demand-supply gap is forecasted to crystallize in the years ahead. By 2050, an impending supply shortfall of approximately 278 million carats looms. (Statista, 2023)

■ India has perpetually been a cornerstone of the diamond industry, with an astounding nine out of every ten diamonds across the globe being polished in the city of Surat.

In a strategic maneuver to counter reduced demand from key markets like the U.S. and the European Union and concerns surrounding diamonds of Russian origin, the Indian diamond industry is strategically recalibrating its focus. It’s now targeting domestic markets and emerging ASEAN economies to tap into latent demand.

■ The diamond’s value metamorphosis from rough to polished to dazzling jewelry is a narrative of dramatic escalation. In a vivid example, rough diamond sales raked in approximately USD 16.4 billion worldwide in 2021, a figure that spectacularly doubled to reach USD 28 billion post-polishing. In 2021, the global diamond jewelry market value was approximately 87 billion U.S. dollars. (Statista, 2023)

■ In 2021, the U.S. accounted for 54% of the world’s polished diamond demand, a significant rise from its 42% share in 2014. (Source: Statista, 2022)

Price statistics in diamond market

■ Unlike precious metals, diamonds lack a uniform market price per carat. Yet, their global prices have embarked on an astonishing journey, expanding over tenfold since 1960.

■ Lab-created diamonds stand as beacons of affordability, consistently priced at 25% to 60% below their natural counterparts.

The dichotomy in pricing trends is distinct: while natural diamond prices have meandered through fluctuations, registering a general upward momentum over the past seven years, laboratory diamond prices have been marked by a steadfast downward trend.

For example. In mid-2018, a 1-carat VS1-clarity, G-color lab-diamond sold for $3,625, compared to the natural version at $6,600. In 2023, prices are $1,615 and $6,705, respectively. Notably, De Beers’ Lightbox has offered a 1-carat lab-diamond of similar quality for just $800 since its launch in October 2018.

■ Between 2021 and 2023, lab-grown diamond prices have decreased by 15-60%, depending on their quality and size.

For instance, a 1-carat lab-grown diamond’s price in Q1 2023 is $1,450, marking a 27% drop from Q1 2021 ($1,980). The trend is more pronounced for larger stones; a 3-carat lab-grown diamond’s price plummeted by over half from Q1 2021 ($20,565) to Q1 2023 ($9,305). (National Jeweler, 2023)

■ Sales of natural diamonds in the global arena, notably in the United States, have trended downward from 2022 to 2023.

In terms of sales, there was a consistent decline on a year-over-year basis, with unit sales decreasing by 10.3% and total value sales falling by 14.0%. Notably, diamond necklaces priced between $1,500 and $9,999 exhibited resilience, with a 1.4% increase in units sold and a 1.6% rise in value. Conversely, all other product categories faced declines.

■ Conversely, the trajectory of lab-grown diamonds is on an upward trajectory. Unit sales of lab-grown diamond jewelry soared by 57.6%, accompanied by a substantial 37.2% surge in value. The average retail price for lab-grown diamond set jewelry demonstrated a pronounced decline, dropping from USD 2,740 in March 2022 to USD 2,405 in March 2023.

Retail statistics in the Diamonds Market

■ In the realm of jewelry adorned with lab-grown diamonds, retailers revel in profits exceeding 50%, a stark contrast to their counterparts selling jewelry with natural diamonds. The allure of higher margins has shifted attention toward lab-grown gems. This transition is being propelled by a considerable reduction in lab-grown costs and prices, incentivizing American consumers to opt for larger lab-grown diamonds.

■ As the year 2023 unfolds, a shift in the landscape of gross profit is evident. Gross profit figures slid from $1,463 in March 2022 to $1,347 by March 2023. Conversely, retailer margins took a promising leap from 53.4% in March 2022 to a more substantial 56.0% by March 2023. The average carat weight per diamond jewelry piece exhibited an upward trajectory, ascending from 1.31 in March 2022 to a notable 1.61 by March 2023. This surge in carat weight hints at an intriguing trend, underpinned by the decrease in lab-grown costs and prices, propelling American consumers toward acquiring larger lab-grown diamonds. (Edahn Golan, 2023)

■ In 2023, the landscape for natural diamonds is marked by mixed dynamics. While the average retail prices of all sold natural diamonds in 2023 continue to outpace their 2022 counterparts, a nuanced decline is noted in the number of diamonds sold, retailer gross margins, and the total value of sales. A closer examination reveals that the first quarter of 2023 saw a decline of 17.8% in the value of US retailer loose diamond sales. In parallel, the number of stones sold experienced an 18.6% year-over-year reduction. These fluctuations spotlight a dynamic market scenario for natural diamonds. (Edahn Golan, 2023)

■ The period between 2020 and 2023 witnessed a threefold increase in the share of lab-grown diamond sales. By value, the share of loose lab-grown diamonds surged from an average of 8.3% in 2020 to a robust 17.3% in 2022. A closer examination accentuates the rapidity of this shift: the value share of loose lab-grown diamonds tripled from 7.2% in January 2020 to a significant 22.9% in February of the following year. This metamorphosis is a testament to the changing preferences of consumers. (Tenoris, 2023)

■ While lab-grown diamonds experience a decline in value post-purchase, a natural diamond manages to retain 50% of its value after the initial acquisition.

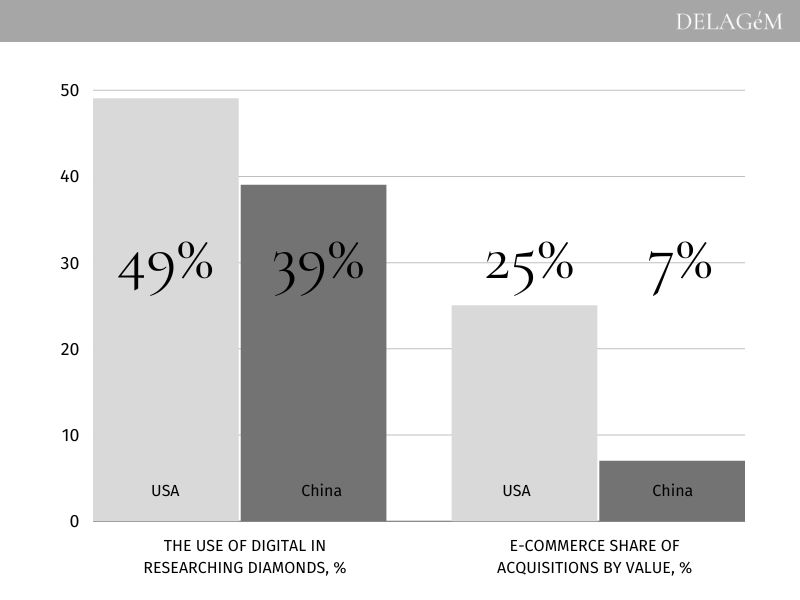

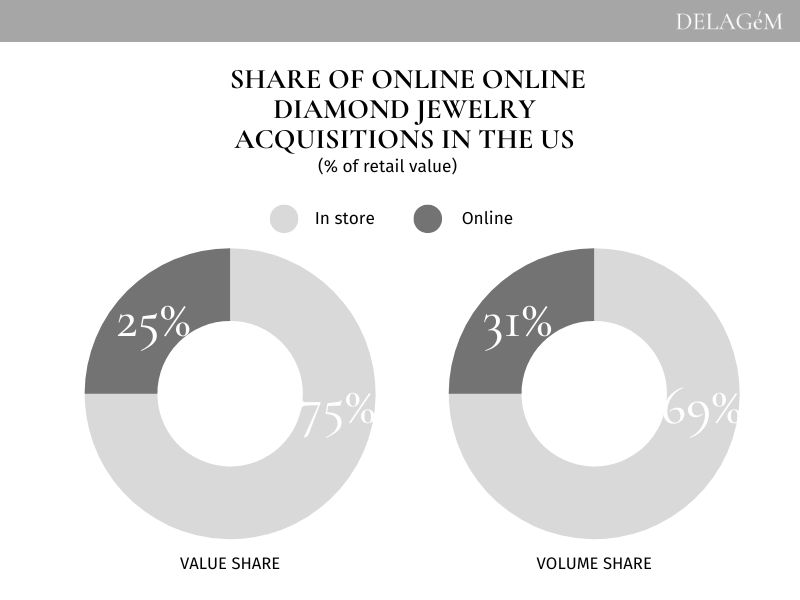

■ Notably, the United States has taken a significant lead in embracing online acquisitions in the diamond domain. In 2021, a substantial 31% by volume of new diamond acquisitions by women and 25% of sales by value showcased an online component. In contrast, the proportions were more modest in China, with merely four percent of acquisitions and three percent of sales value involving an online dimension in 2020. This shift towards online channels is shaping the future of diamond jewelry retail. (DeBeers, 2022)

■ Smaller local designer and retailer brands have surged in growth, capturing a 30% share of acquired pieces in 2019-2021. (DeBeers, 2022)

■ Among Gen Z acquirers, a substantial 42% of acquisitions are made online, a trend mirrored among self-purchasers (40%) and single women (37%). Furthermore, first-time buyers have also displayed significant engagement with online acquisitions, constituting 54% of all online transactions in the United States. These nuances underscore the evolving online acquisition patterns.

■ In the US, the average online sale was $2,204 in 2021, compared with an average of $2,994 for diamond jewelry bought in-store. (Paul Zimnisky, 2023)

Lab-Grown Market Statistics and Facts

■ In 2022, the global lab-grown diamond market was valued at $22.45 billion. Projections indicate a future growth trajectory, with forecasts pointing toward a value of $37.32 billion by 2028, equivalent to 10% of the global diamond market. This surge is set to continue, with expectations of reaching $55.6 billion by 2031, reflecting a compound annual growth rate (CAGR) of 9.8% from 2022 to 2031. These estimates signify the transformative potential of lab-grown diamonds in the diamond market landscape. (Research and Markets, 2023; Allied Market Research, 2023) According to Inkwood Research (2023), the lab-grown diamonds market in Europe is projected to achieve a Compound Annual Growth Rate (CAGR) of 8.85% from 2022 to 2030, with a revenue share reaching $2,977.43 million by 2030. Additionally, Paul Zimnisky (2023) estimated that the volume of lab-grown diamonds produced for the jewelry market was approximately $12 billion in 2022.

■ China and India emerge as global powerhouses in the lab-grown diamond production domain. Estimates place China at the forefront, producing the majority of lab-grown diamonds globally. The combined share of India and China in lab-grown diamond jewelry production is set to dominate, accounting for nearly three-quarters of global production by volume. These production dynamics underline the influential role these countries play in the market.

In 2021, India contributed significantly, producing three million lab-grown diamonds annually, comprising 15% of global output. The Indian government’s actions, like abolishing a 5% tax on imported diamond seeds and funding local diamond seed production, reflect efforts to bolster the sector further.

China reigns as the top producer and exporter of lab-grown diamonds, while India emerges as a prominent global hub. Notably, China held a substantial share of the market, accounting for 56% of the global lab-grown diamond market based on 2019 production.

■ Not all lab-grown diamonds are eco-friendly. They imitate the natural diamond formation process, demanding significant electricity, largely from the national grid. China and India produce over 60% of lab-grown diamonds, utilizing coal for 63% and 74% of their grid electricity, respectively. The diamond-making process can reach temperatures akin to 20% of the Sun’s surface (The Natural Diamond Council, 2023)

Additionally, the notion that lab-grown diamonds are mining-free is a misconception. The synthetic diamond process requires graphite and metals, and the reactors used contain metals sourced from mining operations.

■ Leading lab-diamonds producers include:

Henan Huanghe Whirlwind Co.,Ltd.,

New Diamond Technology Company,

Swarovski International Holding AG,

WD Lab Grown Diamonds,

Applied Diamond, Inc. (Element Six),

HEYARU Group,

ABD Diamonds,

Clean Origin LLC,

Eco Lab Diamonds,

Vibranium Lab Grown Diamonds.

■ Jewelry retailers in Australia, Canada, the EU, New Zealand, the United Kingdom, and the United States, indicate that lab-grown diamonds are diverting business from mined diamonds. An impressive 87% express satisfaction with their decision to embrace lab-grown diamonds due to improved margins and financial prospects.

Nearly all retailers (95%) report better margins with LGD’s versus their mined diamond business with 78% of retailers reporting margins from 16% to 40%+ higher. (MVI Marketing 2022)

Consumer Statistics

■ Consumer preferences highlight the importance of fair-trade labor, ethical sourcing, traceable origin of diamonds and gemstones, and sustainability. About 42% are willing to pay significantly more (up to 25%), and 39% are ready to pay moderately more (up to 10%) for these attributes. (Plumb Club, 2023)

■ In the US, 58% of consumers prefer socially and environmentally responsible diamonds, with 85% overall and 92% among Generation Z willing to pay a premium for such diamonds. (DeBeers, 2022)

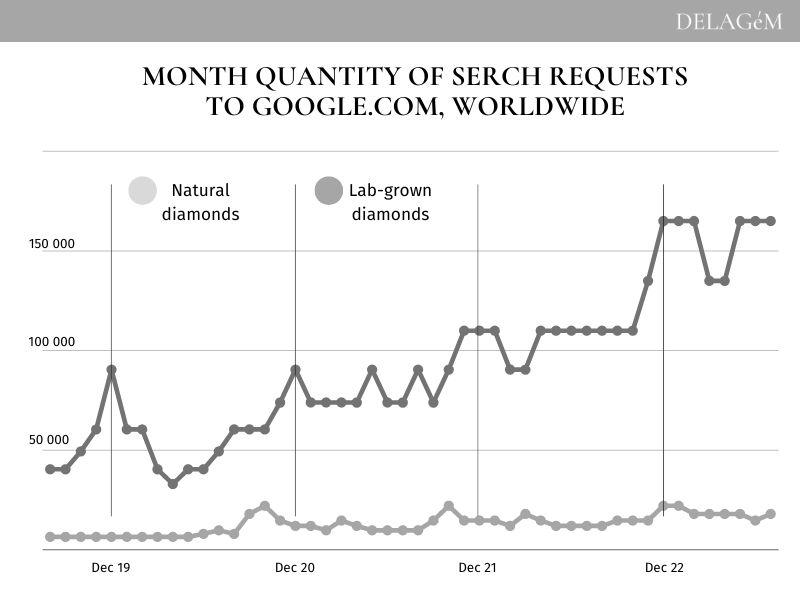

■ As of July 2023, more than 50% of diamonds sold in the U.S. are lab-grown. In contrast, the European Union (EU) market still sees lab-grown diamonds constituting less than 20% of sales. This divergence is largely attributed to the EU’s preference for natural diamonds due to their rarity and resale value, potentially impacting the growth trajectory of lab-grown diamonds in the region. (Read more).

■ Awareness of lab-grown diamonds spans both sides of the Atlantic. In the U.S., 80% of consumers report prior knowledge of lab-grown diamonds, a sentiment mirrored in European nations such as France, Italy, Germany, Spain, and Great Britain, where 77% of consumers were already aware of the product. Interestingly, Italy leads the pack with an 86% awareness rate, accompanied by strong enthusiasm and receptiveness towards lab-grown diamonds. Younger European consumers exhibit keen interest in expanding the lab-grown diamond category, driven by their engagement with social and ethical considerations. (MVI Marketing, 2021)

■ Younger European consumers express a keen desire to expand the lab-grown diamond market. They exhibit stronger engagement in social and Environmental, Social, and Governance (ESG) issues compared to their American counterparts of the same age. (MVI Marketing, 2021)

■ In the US, 36% of consumers are willing to exceed their initial budget for mined diamonds to buy larger lab-grown diamonds. (MVI Marketing, 2022)

■ In Western Europe, 41% of consumers have purchased or received lab-grown diamond jewelry. Among them, 26% are interested in lab-grown diamonds due to lower cost, similarity to natural diamonds, and perceived sustainability. Additionally, nearly 25% value lab-grown diamonds’ larger size for the same price and the inclusion of a grading certificate. (MVI Marketing, 2021) Diamond rings are the most popular jewelry piece, preferred by 45% of customers, followed by diamond pendants or necklaces (42%). (Plumb Club, 2023)

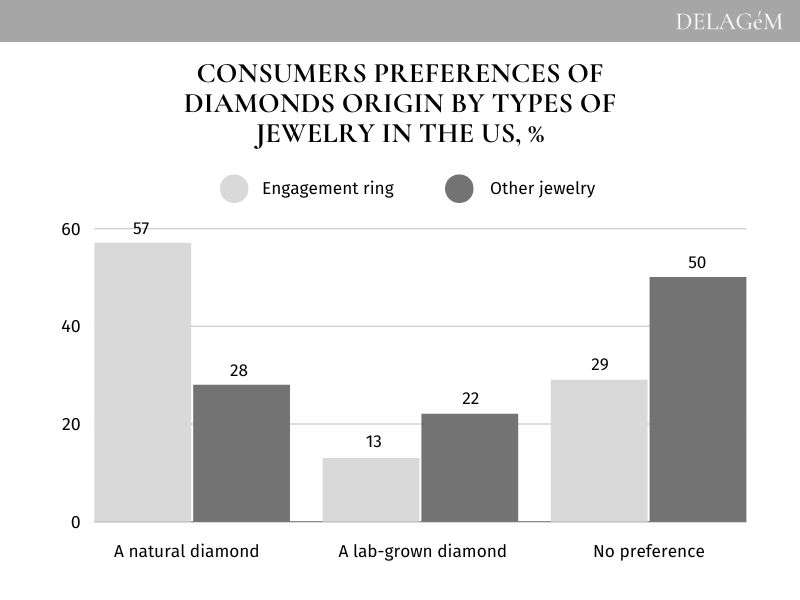

■ When comparing diamonds with the same cut, color, quality, and size, 75% of customers favor natural diamonds. However, 80% are open to receiving lab-grown engagement rings or jewelry from their partners. (Plumb Club, 2023)

■ In the U.S 62% of retailers find that a considerable chunk of their customers, ranging from 5% to 50%, specifically inquire about lab-grown diamonds. (IGDA, 2023)

■ Consumer preferences for diamond jewelry are evident, with diamond rings, pendants, and necklaces being the top choices. Notably, an average of $5,373 is allocated to bridal/engagement pieces, while non-bridal jewelry pieces garner an average spend of $1,297. Moreover, when presented with the option, 80% of respondents express openness to receiving a lab-grown engagement ring or jewelry piece. (Plumb Club, 2023; IGDA, 2023; DeBeers, 2022)

■ High-income US women with incomes exceeding $150,000 display a strong affinity for branded pieces, with 74% of their acquisitions being branded. Similarly, Gen Z and Gen X demographics in the U.S. and China show a predilection for branded diamond jewelry. This alignment of preferences underscores the role of branding in shaping consumer behavior and perceptions. (DeBeers, 2022)

PhD in Economics, CMO and Co-founder Delagem.com